Mortgage Rates Surge as Iran War Stirs Bond Market Turmoil

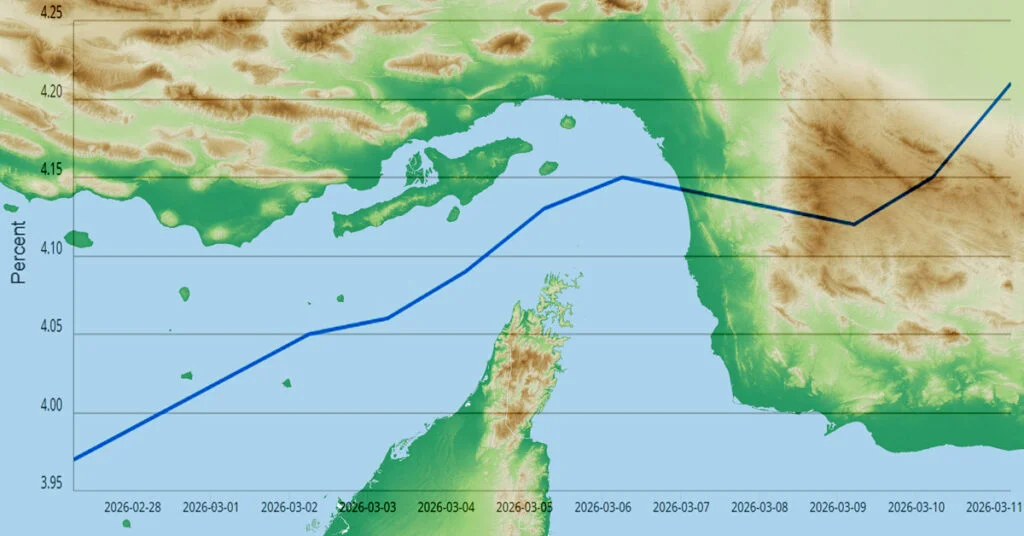

The ongoing war in Iran has sent U.S. Treasury yields to their highest levels since 2007, pushing the average 30-year fixed mortgage rate to 6.72% as of May 18. Data from Mortgage News Daily shows a three-quarter percentage point jump from pre-war levels, with 10-year Treasury yields peaking at 4.69% on Tuesday before retreating to 4.58%. The spike reflects deepening inflation fears driven by a global oil shock, which has raised energy prices and spilled over into broader consumer costs such as groceries.

According to ABC News, the yield on 30-year bonds touched their highest point since 2007, while 10-year yields climbed about three-quarters of a percentage point since the conflict began on Feb. 28. Ted Rossman, a senior industry analyst at Bankrate, told ABC News: “It’s really all about the Iran war and its inflationary impact.” The soaring bond yields have made borrowing more expensive across the board, including for mortgages, credit cards, and auto loans.

The mechanism is straightforward: regulated lenders must hold reserve assets like U.S. Treasuries, and when Treasury yields rise, the cost of holding those assets climbs. Lenders then pass these higher costs onto consumers. “The bank will pass along that higher cost of capital to any consumer loan,” Patrice Carrington, a professor of real estate at New York University, explained to ABC News.

Why Borrowers Face a Sharp Squeeze — and a New Choice

For homeowners and would-be buyers, the immediate impact is clear. Each percentage-point rise in mortgage rates adds hundreds of dollars to monthly payments. With rates now at 6.72%, many are feeling the pinch — especially as housing inventory remains tight. The stakes are high: for someone financing a $400,000 home, the difference between a 4% and a 6.72% rate is nearly $700 more per month.

Yet the crisis has also reshaped the mortgage landscape in unexpected ways. In the U.K., tracker mortgages — where the interest rate moves in line with the Bank of England base rate — have surged in popularity. At current levels, trackers are now cheaper than fixed-rate deals, reversing a long-standing trend. Mortgage broker L&C Mortgages reports that applications for trackers in April were more than three times higher than in March. “They are back in the conversation,” said Nicholas Mendes at broker John Charcol, as reported by The Guardian.

The shift stems from the same inflationary pressures. Concerns over higher oil and gas prices have pushed up swap rates that lenders use to price fixed mortgages, making tracker deals comparatively attractive. As The Guardian notes, “now the best-buy deals are dearer than the cheapest trackers.” The Bank of England has left its base rate at 3.75% since a cut in December, but warned that the Iran conflict could force rates up to 5.25% by early 2027 if inflation persists.

For borrowers, the calculus is nuanced. Tracker mortgages often come with no early repayment charges, allowing borrowers to switch to a fixed deal later if rates fall. “If fixed-rate deals become cheaper in a few months, you could then hop on to one of those,” The Guardian reports. However, the risk is equally real: if rates rise, monthly payments will climb. “A lot depends on whether you can afford to be wrong — that is, if rates were to rise, would you be able to afford your mortgage?” advised Mark Harris of broker SPF Private Clients.

Broader Economic Shockwaves and Lingering Uncertainty

The war’s inflationary impact extends well beyond mortgages. The bond market selloff — triggered by expectations of higher energy costs — has raised borrowing costs for credit cards, auto loans, and even corporate debt. This compounds the pressure on households already grappling with higher prices at the pump and grocery store. The economic climate echoes the aftereffects of President Donald Trump’s “Liberation Day” tariffs in April 2025, which also sent yields spiking. This time, the trigger is a geopolitical conflict that shows no signs of quick resolution.

In the U.S., the housing market has been particularly slow to adapt. Record Memorial Day travel is expected despite high oil costs topping $4.50 a gallon, signaling that consumers are still spending — but some of that spending may come at the expense of home-buying plans. Meanwhile, the war’s impact on global markets has been compounded by other tensions, such as Russia hitting Kyiv with hypersonic missiles in a massive attack, adding to uncertainty.

For borrowers, the key question is whether to lock in a fixed rate now or take a gamble on a tracker. Some analysts see trackers as a reasonable “holding position” until the outlook clarifies. But the Bank of England’s worst-case scenario warns that rates could rise to 5.25% by early 2027, which would make trackers far more expensive. Conversely, if the war ends quickly — as some diplomatic signals from Secretary of State Marco Rubio hint — base rates could stay flat, making trackers a bargain.

On a broader level, the bond yield surge signals that inflation is not yet tamed. The Federal Reserve and the Bank of England both face a difficult balancing act: raising rates to curb inflation could strangle growth, but doing nothing risks embedding price increases. For now, borrowers are left navigating a volatile landscape where the only constant is change. As Rossman concluded, “That’s a really big jump.” The question is whether it’s the start of a longer climb or a temporary peak.

Comments